Co-Authored by Matt Frommer, Housing Forward Colorado, and Luke Teater, Thrive Economics

One common myth about new market-rate housing is that it’s all “luxury housing for rich people.” Those who make this argument often acknowledge that we have a housing affordability crisis, but insist that changing zoning laws to allow more market rate homes “won’t help” because none of the new housing will be affordable. At first glance that may sound plausible, but it deserves a closer look.

New apartments are affordable for most households

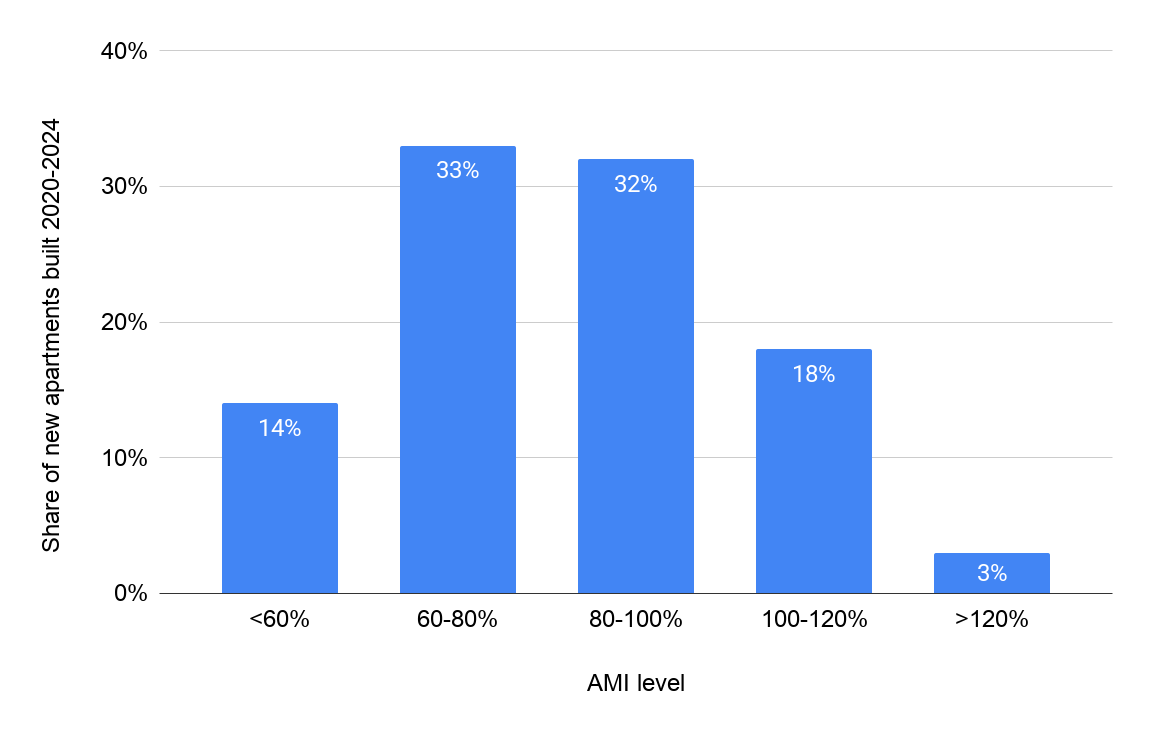

Census data shows that most apartments built in the last five years are relatively affordable for households across the Denver metro area. Nearly 80% of rental units built from 2020 to 2024 are affordable to households earning the area median income (100% of AMI). Put differently, a family in the middle of the income distribution can afford 80% of apartments built since 2020, suggesting the vast majority of these homes are not what most people would call “luxury.” According to the US Department of Housing and Urban Development (HUD), a home is affordable if the residents pay no more than 30% of their income on housing costs.

Share of new Denver-area rental units built 2020-2024 by income level they are affordable to (AMI)

In addition, nearly half of apartments built since 2020 are affordable to a two-person household earning about $84,000 per year, equivalent to 80% of Denver’s AMI, which HUD classifies as “low income.” In high‑cost regions like Denver, workers like teachers, bus drivers, restaurant workers, nurses, and childcare providers often qualify as “low income” under housing rules – largely because local housing costs have risen faster than their wages. So it’s especially notable that much of the new housing is affordable to households earning between 60% and 80% of AMI. That group is often left out of traditional affordable housing programs, which tend to target households earning 60% of AMI or below. In other words, new market-rate housing is workforce housing.

Yes, there are some new high‑end buildings with rooftop jacuzzis and pet spas, but the data show that just 3% of recently-constructed apartments are affordable only to households making over 120% AMI: $125,280 or more for a household of two. Some of that 3% are truly luxury units and reflect properties that are pursuing a different business strategy and tenant base than most apartment owners, as shown by their median rent of $6,018 per month.

New apartment rents are very similar to existing apartment rents

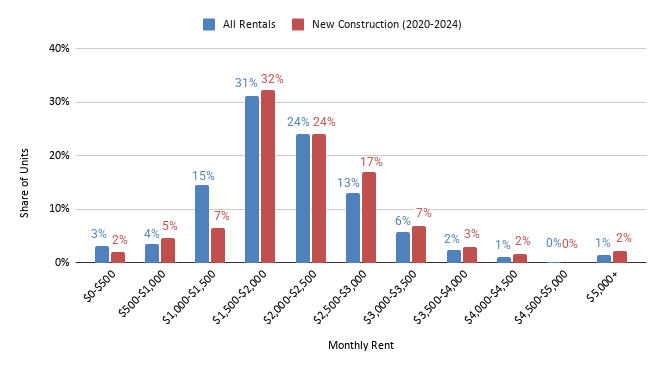

For the most part, new apartments rents look remarkably similar to those across the broader rental market. Nearly half of Denver’s newly built apartments rent for less than the median rent for all units in the metro area.

The graph below compares monthly rents for new apartments built since 2020 (red) with all apartments in the city (blue). If all new apartments were “luxury” housing, we would expect to see taller red bars on the right side of the graph at higher rent levels. Instead, the distribution of new apartments is remarkably similar to that of the overall rental market.

Source: 2024 ACS PUMS household microdata from IPUMS for the Denver-Aurora-Lakewood metro area.

For both new and existing rental housing, the most common rent range is $1,500–$2,000 per month. In Denver, that roughly corresponds to 60–75% of AMI for a one-bedroom apartment and 50–65% of AMI for a two-bedroom apartment. We suspect that many of the apartments renting for less than $1,500 per month – both existing and new units – are deed-restricted affordable housing.

New supply is bringing rents down across the board

Not only are new apartments relatively affordable, but the historic amount of new supply is driving down rents for all housing in Denver, especially for lower‑income families. In 2025, Denver metro rents fell 7.2% overall and 11.5% for Class C apartments – the older, more affordable segment of the market that typically houses lower‑income families. That’s because as new supply comes online, it allows some households to “trade up,” moving into larger or newer units for similar monthly costs. Those moves free up older, less expensive units for others, creating a ripple effect known as “moving chains.” Even if a new building doesn’t look affordable at first glance, adding homes at the top or middle of the market helps relieve competition for limited options at the bottom. Our previous blog post covers this phenomenon in more depth.

The relative affordability of new rental housing is producing another outcome. In some cases, taxpayer-subsidized affordable housing is competing with market-rate housing delivered at no cost to taxpayers. As a result, owners of affordable housing developments are struggling to lease their units. The vacancy rate for income-restricted units for households making 60% of AMI is 12.8% compared to 8.3% for market-rate apartments. This isn’t to suggest we don’t need subsidized housing, but it may be worthwhile to revisit the policy design to more efficiently deliver affordable housing for very low-income families that aren’t served by the market.

To recap, new market-rate housing is affordable for most households and also helps lower rents across the market. Therefore, policies that enable more market-rate multifamily housing should be considered core affordable housing solutions. In reality, “luxury housing” may be more of a marketing term than a description of who actually lives in the vast majority of new homes in the Denver area.

The risk of slowing production

Unfortunately, construction has slowed dramatically because of higher interest rates, rising construction costs, and softening rents (less profit opportunity for developers). If this trend continues, we should expect rents to climb again in 2027 and 2028, with the sharpest increases likely in the most affordable parts of the market. To get renters off this rollercoaster of price shifts, Colorado needs steady, sustained housing production so that homes remain attainable over the long run.

Cities should take steps to support more multifamily housing development in their communities, and many already are. Fort Collins, Wheat Ridge, Denver, and Longmont are early movers in complying with Colorado’s Transit Oriented Communities (TOC) law, HB24-1313, encouraging more multifamily housing near transit. As a result, they were rewarded with a combined $13 million in state TOC Infrastructure grants to help unlock more housing development near transit. More recently, Arvada launched its Livable Center in Transit-Oriented Communities project to expand housing options near transit.

Everything discussed above is specific to the rental market, which has seen meaningful price reductions due to record levels of new apartment supply. The same cannot be said for the homeownership market. This is partly due to the limited number of multifamily condominiums coming online for purchase, but it is also a result of exclusionary zoning policies that reserve most residential land for single-family homes on large lots and prohibit affordable “middle housing” options like townhomes, duplexes, and cottage courts. In practice, this means many communities are legally constrained from adding more for-sale housing – regulations that need to be reformed if we want to see similar success in the homeownership market as we’ve seen in the rental market. Fortunately, communities like Denver, Aurora, and Boulder are pursuing reforms to allow more affordable middle housing types in existing residential neighborhoods – policy changes that have proven to expand homeownership opportunities in other cities like Portland.

Housing is a regional issue, but individual cities each have a role to play. By allowing more housing types and dramatically increasing supply, cities can help lower housing costs, not just for new homes, but for existing homes as well.

*This analysis uses 2024 ACS PUMS household microdata from IPUMS for the Denver-Aurora-Lakewood metro area. The “new rental” sample includes occupied renter households in units reported as built in 2020 or later, with positive gross rent. The sample includes 221 unweighted observations, representing about 31,300 renter households/units after Census weighting. We compare those rents with all renter households in the same geography and with 2024 CHFA/HUD AMI rent thresholds. We use 2024 AMI levels to match the rent data from the 2024 Census. 80% of AMI in Denver for 2026 is up to $92,160 per year according to the Colorado Housing and Finance Authority (CHFA).

To receive news and analysis from HFC, subscribe at the bottom right of this page!